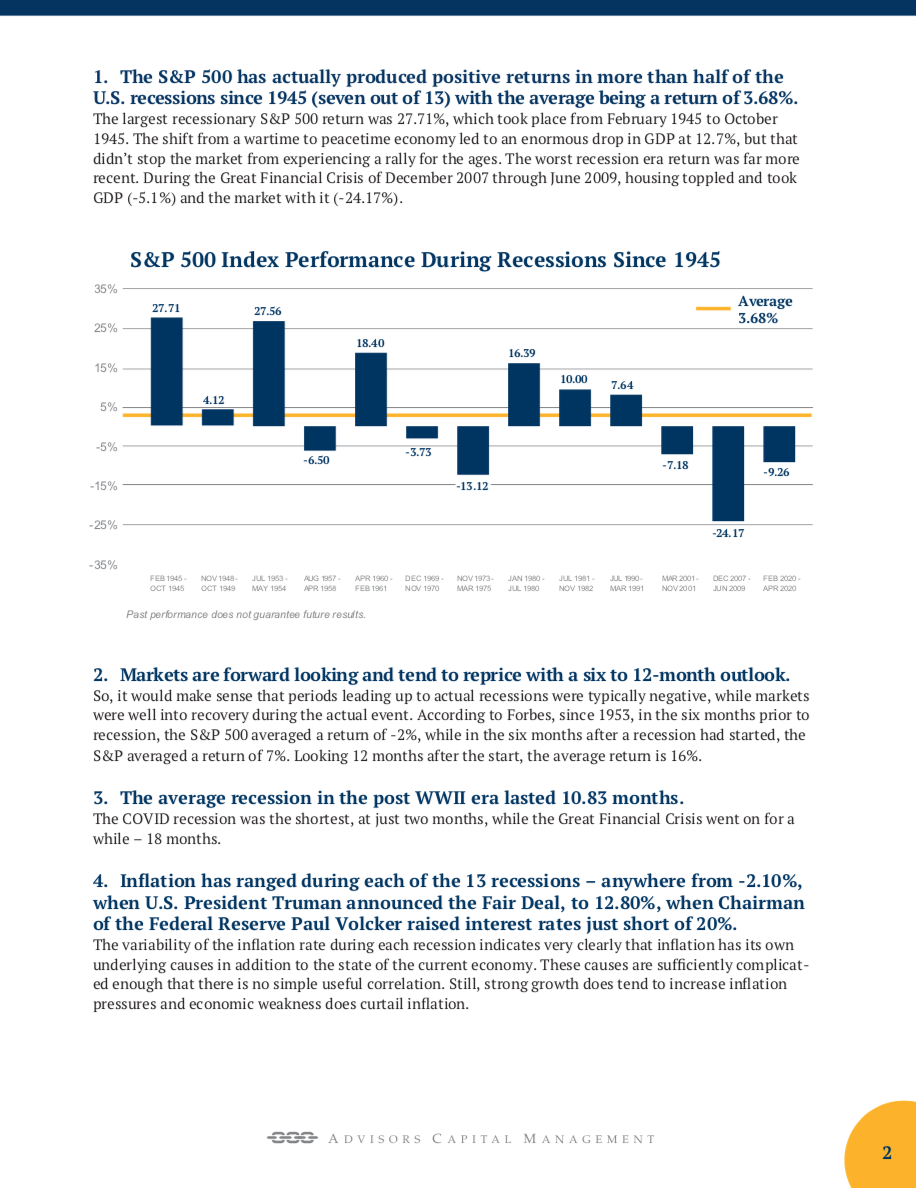

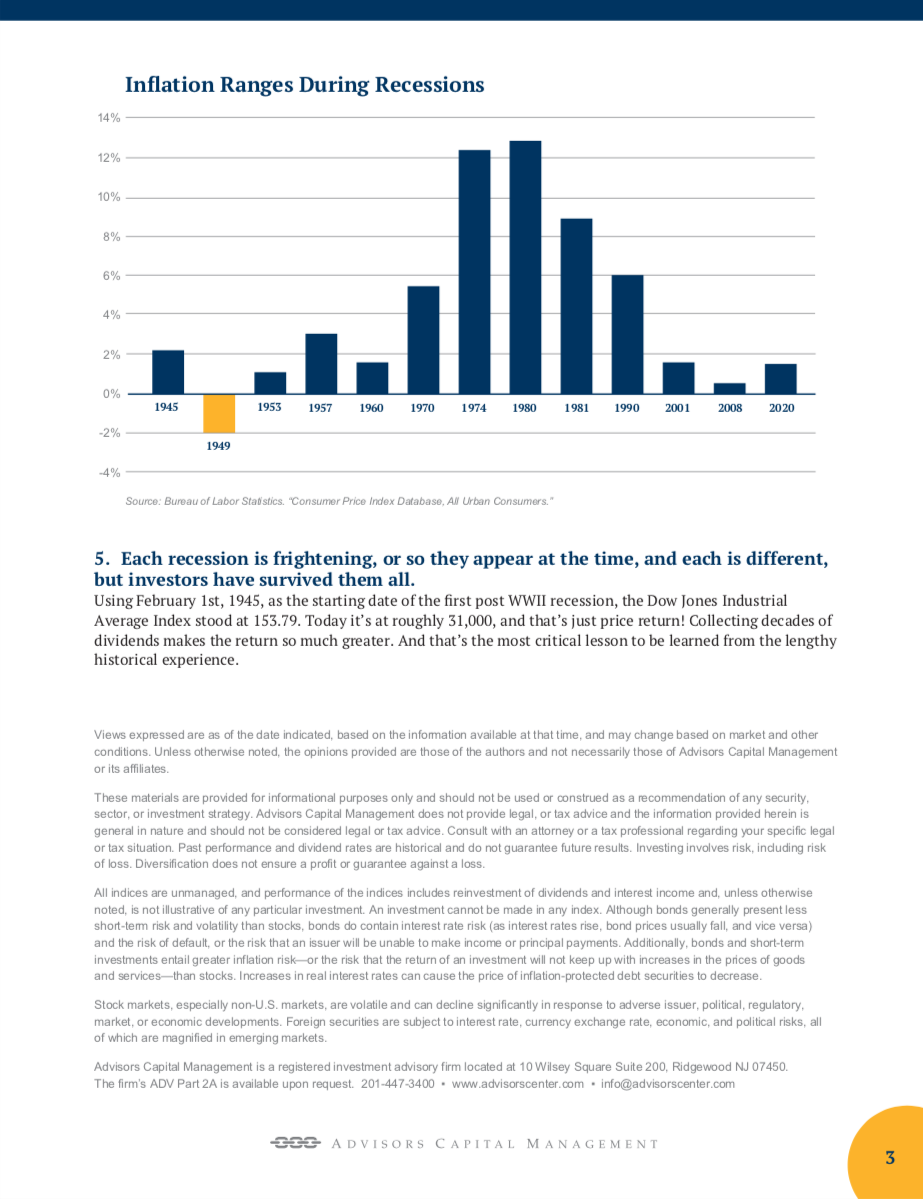

SUBSCRIBE TO OUR NEWSLETTER

Receive news and updates (no spam!)

Sizable decline in stocks and bonds reflects the shock to many investors who thought inflation would be tamed easily and must now accept that the Fed may be forced to raise interest rates more than commonly believed. While the Fed only recognized the problem after an inexcusable delay, it now appears fully committed to bringing inflation back to target. As they say, “Don’t bet against the Fed.” What remains unclear is just how much rates needs to rise. We expect policy rates to rise continuously until they bring inflation to heel.

Market hopes were quickly dashed for a near-term significant reduction in inflation towards the Fed’s roughly 2% objective. Inflation is running hotter than widely expected and it is broadening out and becoming more pervasive. In fact, the bond market is still not priced properly. For growth to slow sufficiently to bring down inflation, it is likely necessary for rates to rise somewhat above the rate of inflation, at least those parts of inflation that aren’t transitory. Until rates rise accordingly, negative real interest rates will be promoting growth rather than restraining it. Since inflation is running well above 4% even when stripped of those transitory factors, such as new and used car prices, shipping costs, and chip prices, market long-term financing rates almost certainly need to exceed that level. The good news is that we’re not that far away at this point.

Likewise, stocks are already far along to repricing to reflect these realities, with high P/E multiple and unprofitable companies bearing the worst of the carnage, as they should. 47.8% of NASDAQ Composite stocks are down at least 50% from their recent peaks, 25.7% are down more than 75% and 6.4% are down at least 90%. While the markets are likely to remain volatile over the coming months, valuations have fallen enough that many stocks can now be regarded as cheap and already, to a debatable degree, are priced for a potential recession. The S&P 500 is now trading around 17 times projected earnings, which means that many good companies trade below 12 or even 10. While we suspect the worst of the decline is behind us, stock prices commonly overshoot, so some additional declines should be expected. Rather than sell out at depressed prices to protect against any remaining downside, our view is that it is a time to reassess the prospects for companies and to swap into those that have been treated too harshly by investors. Indeed, corporations seem to share this judgment and stock buybacks are proceeding at record rates.

Fears of recession are, of course, a key component of the stock market decline, yet no recession is imminent nor is one assured. Fear mongering is also rampant, which is all too normal. In the most recent employment report, businesses added 390,000 net new hires, a number inconsistent with recession and far too high to be sustainable. There are simply not enough unemployed bodies around to continue adding new workers at this pace, even though there are still more than 11.4 million job openings. So, we expect hiring to slow considerably and expect this to show up in the data in the months immediately ahead. (In fact, it would slow even if the Fed did absolutely nothing.) The Fed needs to get hiring below 100,000 to ease some of the wage pressure that underlies inflation. Yet, some will argue that any decline in hiring is merely a step along the way to recession, despite the strong support underpinning major sectors of the economy.

Key parts of the economy are still constrained by supply bottlenecks. While some analysts focus on the rise in mortgage rates inhibiting housing, homes for sale and apartments for rent remain overly scarce and builders lack the labor and building supplies to increase production. Even worse, it will take a number of years for builders to catch up with demand after more than a decade of underbuilding. Thus, we expect housing construction to outperform considerably its historic sensitivity to higher mortgage rates. Similarly, auto production has some catching up to do after supply disruptions due to chip shortages. Capital investment will also benefit as the world shifts production closer to home after just-in-time production and globalization proved vulnerable to disruption. National defense spending will provide yet another source of demand. If the economy does lapse into recession, which is by no means obvious, it is likely that any downturn would be fairly mild.

It is easy to be gloomy with inflation running at levels not seen since the 1970s amid so much international and domestic political conflict. This is plenty to be gloomy about. But gloom doesn’t trigger recession, even if it does induce more people to follow the news. If so, we would never recover from recessions that are chock full of gloom. Instead, there are key developments yet to play out that could have very positive or negative consequences. It seems unlikely, but some of the gloom and inflation pressures could be lifted quickly if the government announced plans to suspend some of its anti-fossil fuel initiatives, even if only temporarily. The Treasury and the Fed have numerous cards to play. As investors, we must remain highly vigilant, so we can adapt quickly to new developments. Most assuredly, it is likely that there will be surprises aplenty.

The foregoing content reflects the opinions of Advisors Capital Management, LLC and is subject to change at any time without notice. Content provided herein is for informational purposes only and should not be used or construed as investment advice or a recommendation regarding the purchase or sale of any security. There is no guarantee that the statements, opinions or forecasts provided herein will prove to be correct. Past performance may not be indicative of future results. Indices are not available for direct investment. Any investor who attempts to mimic the performance of an index would incur fees and expenses which would reduce returns. Securities investing involves risk, including the potential for loss of principal. There is no assurance that any investment plan or strategy will be successful.

By Dr. JoAnne Feeney, Portfolio Manager

The headlines of late have indeed been worrisome, whether it be high inflation, rising interest rates, China’s zero-Covid policy, or war in Europe. (But that is the nature of headlines.) Market risks remain above normal. Elevated risk and higher interest rates tend to lower stock valuations, while higher future earnings raise valuations. We have seen many stocks decline because of the former, but we are now entering a period where earnings fundamentals have the chance to dominate the narrative as companies report first quarter results and provide guidance for 2Q and the full year. Should we expect good news and how much should it matter?

When companies reported their 2021 results earlier this year and provided guidance, many turned cautious and more companies cut guidance than not. Omicron was causing a spike in Covid cases, and consumers were pulling back on activities. Companies noted elevated risks and pointed to ongoing supply chain issues, but they also remarked that Omicron would be short-lived, the supply chain was starting to improve, and the second half of the year should be better. Investors remained skeptical.

Now, three months on, companies have seen Omicron fade, but other disruptions have come to the fore. Russia’s invasion triggered sanctions, reduced exports of metals and grains from that region, and worsened the global shortage in the supply of oil. China’s zero-covid policy once again disrupted the production of consumer electronics and cars and slowed the flow of products in and out of Chinese ports. Statements by Federal Reserve officials imply that several rate hikes lie ahead. And CPI inflation hit a hew high.

Understandably, we shouldn’t expect much optimism from companies regarding sales and earnings for this quarter, but the state of the US economy suggests we may very well hear indications of improving growth prospects for the second half of the year. As our Chief Investment Officer, Chuck Lieberman, wrote a couple of weeks ago, it is premature to anticipate recession, regardless of headlines to the contrary, because the US is unambiguously still in expansion territory (and has a long way to go). Now that earnings season is upon us, we will hear from companies as to the conditions they are seeing on the ground. More importantly, we will get clues on their positioning for the rest of this year and whether they are likely to be able to power through these macro risks.

Last week may have started out with those high inflation numbers, but it finished with a very strong read on US manufacturing. Friday’s Industrial Production report came in better than expected with output up 0.9% month over month versus an expected 0.6%. This strength was driven by greater production of autos (as shown in lower half of chart) and business equipment. Moreover, capacity utilization is up to 78.7% from 78.1% in February; it is the highest it’s been since 2007 (but has room to increase further). Firms are having some success filling job openings. This matters because more workers enable factories to run hotter and provide households with more income to boost spending. This creates a positive backdrop as we are likely to hear from companies over the next several weeks.

So, while the recent narrative has been all about the macro negatives—especially high inflation and rising rates— now it’s earnings chance to dominate the news, as companies begin reporting first quarter results and provide guidance for 2022. While risks and rates can only go so high, earnings can keep going higher year after year after year. This is the critical force behind the attraction of long-term investing that has powered the S&P 500 up over 1,000% over the last 30 years. While we should be prepared to hear continued near-term caution, we need to focus more closely on the clues companies provide on plans that will drive the longer-term trajectory of their sales and earnings. And because we are in a period of elevated risk, while we position portfolios to take advantage of both cyclical and secular growth, we are also building in holdings that will do well even as inflation, rates, and geopolitical tensions remain high.

The foregoing content reflects the opinions of Advisors Capital Management, LLC and is subject to change at any time without notice. Content provided herein is for informational purposes only and should not be used or construed as investment advice or a recommendation regarding the purchase or sale of any security. There is no guarantee that the statements, opinions or forecasts provided herein will prove to be correct. Past performance may not be indicative of future results. Indices are not available for direct investment. Any investor who attempts to mimic the performance of an index would incur fees and expenses which would reduce returns. Securities investing involves risk, including the potential for loss of principal. There is no assurance that any investment plan or strategy will be successful.

About the Author

Dr. JoAnne Feeney

Dr. JoAnne Feeney is a Portfolio Manager and a member of the investment committee with Advisors Capital Management, LLC (ACM). Prior to joining ACM, Dr. Feeney was senior equity analyst for more than 10 years at boutique sell-side firms including…

Stories abound regarding the impending recession, either as signaled by the inversion of the yield curve or due to excessive Fed rate hikes to contain inflation, take your pick. I can’t figure out if the recession forecast is reckless or just incompetent economics. Strong growth continues unabated, as shown by the latest jobs report. But it is highly premature to project recession when the Fed’s rate hikes have barely begun.

It is historically correct that an inversion of the yield curve, where shorter maturities offer more yield than longer maturities, commonly precede every recession. However, not every inverted curve is followed by a recession. Moreover, when an inverted curve is followed by a recession, the time lag between the inversion and the subsequent recession has been extremely variable, as little as six months and as long as two to three years. The value of such a forecast is comparable to that of a weather forecaster predicting snow in July.

In theory, a yield curve inversion does predict a decline in interest rates. Moreover, if the calculations are done carefully, it is possible to tease out when the market expects rates to fall and even by how much. The critical missing variable that makes the calculations imprecise is the unknown value of the term premium, which is how much extra yield investors require to hold longer maturity debt. Normally, a 2-year bond should yield more than a 1-year bond. Longer maturity debt exposes investors to far more unknown future developments, protracted negative effects on buying power due to inflation, and other considerations that all justify investors getting a higher yield for owning a longer maturity bond. So, when the yield curve inverts, it follows that the market expects rates will fall by more than that unknown term premium. That’s the theory.

In practice, numerous factors weigh on investor behavior, with today’s wild card being how much the Fed’s quantitative easing has distorted the messaging system embedded in the yield curve. The Fed owns about one-third of all the Treasury debt outstanding, including the longest maturities. If the Fed allows its oversized bond portfolio to run off by choosing not to reinvest in new bond issues, the Fed is really reducing mostly short-term debt, not long-term holdings. With long-term, high-quality debt still scarce in the marketplace, those rates would remain artificially low, which was precisely the Fed’s original intention. The Fed wanted long-term rates to become depressed to promote risk taking and economic recovery. If so, there’s not much forecasting power implied by the inverted curve. Rather, it is a very imprecise indication that the Fed has greatly distorted the market signals of an inverted curve.

Yet equally critically, there is precious little logic that an inverted curve predicts recession when the absolute level of rates remains so low. Consider a 2-year corporate bond yielding 3.5% while a 10-year corporate bond yields 3.0%. Under these circumstances, companies would be strongly incentivized to borrow great sums for 10 years for any and all future known and unknown needs and to invest the cash they raise in shorter maturities to earn a positive spread. They can raise extra cash now and earn a return while they wait for good investment opportunities to appear. And when they need the funds to pay for capital investment, they can just allow those shorter maturities to mature. Such behavior would lengthen the business cycle, not curtail it.

In the meantime, economic growth remains robust, as is crystal clear from the latest jobs report. There are some people re-entering the labor market from the sidelines, which is helpful to moderate wage growth. But this added labor supply is still being overwhelmed by labor demand. Job openings remain above 11 million, even as unemployment is falling. So, the labor market continues to get tighter. The ratio of job openings to the number unemployed has soared to a record peak vastly outstripping all past levels, as shown in the figure below.

Hand wringing over the inversion of the yield curve is mostly just a distraction. The real problem is growth remains too strong. What remains unclear is whether the Fed can steer the narrow course between raising interest rates too slowly, so that inflation remains far above target, or raising rates too much, pushing the economy into recession. The Fed’s track record on finding this middle ground isn’t very good. So, there are views on both sides of this debate. It is our judgment that it is still premature to predict the outcome, since the Fed is so early in trying to contain inflation. So, we will track its policy actions very closely.

The foregoing content reflects the opinions of Advisors Capital Management, LLC and is subject to change at any time without notice. Content provided herein is for informational purposes only and should not be used or construed as investment advice or a recommendation regarding the purchase or sale of any security. There is no guarantee that the statements, opinions or forecasts provided herein will prove to be correct. Past performance may not be indicative of future results. Indices are not available for direct investment. Any investor who attempts to mimic the performance of an index would incur fees and expenses which would reduce returns. Securities investing involves risk, including the potential for loss of principal. There is no assurance that any investment plan or strategy will be successful.

Some of you may have had flashbacks to the late 1970s when you saw the latest CPI inflation report last week. At a 6.8% year-over-year increase, US consumer prices have not risen that rapidly in nearly 40 years. Even excluding the more volatile energy and food components, the U.S. saw Core CPI rise 4.9%. Moreover, the shortages driving inflation ever higher appear unlikely to ease anytime soon, and we are only starting to see rising housing costs filter into measured inflation figures. Core inflation could get worse before it gets better, even if the headline pace drops with lower energy prices, as seems likely. Investors worry that inflation itself, and the response of the Federal Reserve, may spoil prospects for continued appreciation in equities, but a deeper look suggests attractive opportunities for equity investing remain firmly in place, although positioning for higher inflation risks is needed.At the heart of rising prices is simply lots of demand and too little supply. A quick reminder—this is still not anything like the stagflation we saw in the 1970s-80s. The US economy is growing very robustly – just not enough to meet all that demand. That growth is a plus for company sales and profits (and so for equities), and it is widely understood that year-over-year growth will slow in 2022. The growth rate of 2021 is simply too high to be sustainable and reflects abnormally low production in 2020, yet growth in 2022 appears likely to remain above trend as supply chains continue to recover. Rising employment and strong household balance sheets support spending, but supply increases have been limited by COVID, related shutdowns, and supply chain bottlenecks. Moreover, the shortage of labor, after many left the workforce during the worst of the pandemic and have stayed out, is driving up wages and this is feeding into prices. Yet despite this, many companies—but not all—are finding that consumers are willing to pay higher prices and so are maintaining record profit margins.

Investors and policy officials, however, wonder for how long companies and consumers can manage a high inflation environment. If the Fed can take some of the pressure off prices by encouraging consumers to defer spending for a while—just until supply can catch up—it could deliver that elusive “soft landing” wherein growth remains robust, incomes continue rising, unemployment falls, and inflation returns to more normal levels. That may be a very tall order.

The fundamental solution to high inflation—beyond Fed tightening—is for supply to catch up to demand. We are seeing some easing in shortages in semiconductors, for example, as automakers finally have all their North American plants operational again. But more broadly, labor shortages may limit the pace of supply growth, even as other material and component shortages abate. Last week’s reported unemployment claims hit a low not seen since 1969 (and U.S. population has grown more than 50% since then). Job Openings continue to climb, but Quits remain stubbornly high as workers job hop to take better paying jobs, and this makes it hard for firms to make much headway in filling positions.

One outlet for excess U.S. demand has often been through higher imports. The bottlenecks at two of the country’s largest ports, in LA and Long Beach, had appeared to be easing. Fewer ships were lined up to be unloaded. It looked as though transportation networks were getting better at unloading ships, distributing their goods to warehouses, and delivering all that stuff to consumers. Turns out very little has changed at the ports, except the location of many of those waiting ships. They are now simply parked farther out to sea, out of the range of those doing the counting. Port watchers are now saying we have not even reached the peak of port backups, let alone started to see those bottlenecks ease. The pileup at our ports indicates that demand remains robust (a plus for equities) although also suggests we are unlikely to see much easing of inflationary pressures via imports until well into 2022.

The Fed will try to dampen demand by tapering and raising rates, since supply is pretty much beyond its control, but low global interest rates may, unfortunately, limit the Fed’s ability to move U.S. rates higher. While this would leave inflation running above target for much longer than desired, it would also reflect firms continuing to sell into a very strong demand environment. It appears we are destined either to live with higher inflation or higher interest rates, and likely, a combination of the two for the foreseeable future. The implication for equity investing is to build portfolios accordingly to balance those risks—some real estate, financial, and energy companies, and certain secular growth companies that can offer an inflation hedge or thrive in a higher inflation and rate world.

The foregoing content reflects the opinions of Advisors Capital Management, LLC and is subject to change at any time without notice. Content provided herein is for informational purposes only and should not be used or construed as investment advice or a recommendation regarding the purchase or sale of any security. There is no guarantee that the statements, opinions or forecasts provided herein will prove to be correct. Past performance may not be indicative of future results. Indices are not available for direct investment. Any investor who attempts to mimic the performance of an index would incur fees and expenses which would reduce returns. Securities investing involves risk, including the potential for loss of principal. There is no assurance that any investment plan or strategy will be successful.

Dr. JoAnne Feeney is a Portfolio Manager and a member of the investment committee with Advisors Capital Management, LLC (ACM). Prior to joining ACM, Dr. Feeney was senior equity analyst for more than 10 years at boutique sell-side firms including…

About the Author

That was the strongest “weak” jobs report I’ve ever seen. While payroll jobs increased by “only” 210,000, far less than the 500,00 plus expected, the household survey reported job gains above 1.1 million, while the unemployment rate plunged, despite a surge in labor force participation. The economy is running very hot. Fed Chair Powell deep sixed the term “transitory” to describe inflation and it is very likely the Fed will announce an increase in the pace of tapering its bond buying at its upcoming meeting.To put things into better perspective, 210,00 payroll jobs is roughly three times the underlying growth of the labor force. So, it was hardly weak. Rather, it was disappointing, since a much larger job gain was expected. But no one could have been disappointed with the lights out job increase reported in the household survey of 1.136 million. Moreover, the labor force participation rate surged by 0.2%, which added 594,000 people looking for work. These new job seekers were snapped up, plus another 542,00 previously unemployed, so the unemployment rate plummeted to 4.2%. The Fed’s latest forecast projected a 4.6% unemployment rate for December. Every other measure we have of the U.S. labor market is extremely strong, which is why (net) job growth of 500,000 was widely expected, but this report really lived up to that high expectation.

Policymakers at the Fed now have to re-evaluate the current policy approach. Several have already stated publicly that a faster reduction in bond buying is appropriate. We agree. Counting noses, we suspect Powell knows this is coming and has even suggested he supports it. If they double the monthly reduction in bond buying from $15 to $30 billion, they will complete the program by March instead of June. That will open the door to an earlier start to policy rate hikes. With inflation running hot, strong economic growth and some fiscal stimulus coming with more possibly on the way, it is long past time for the Fed to put its emergency bond buying program to bed.

This positive economic scenario can still be upended by Omicron. The little information we have suggests that Omicron may be more contagious than Delta, but less severe. And it appears that those already vaccinated have only mild cases of illness, at least so far. If the current vaccines provide some protection against Omicron, then boosting antibody levels with additional booster shots may be sufficient to bridge the period until new vaccines designed for Omicron become available. Once again, it appears that only the unvaccinated risk serious illness. But these are highly preliminary judgments based mostly on anecdotal reports. Firm conclusions are premature. Some early Omicron research results should become available within a few weeks. In the meantime, it appears that the pace of vaccinations has increased considerably, now running over 2 million per day over the past few days, which will be helpful no matter what the test results. It is doubtful that governments will require another round of shutdowns, but people may turn more cautious if Omicron proves to be more dangerous. By the same token, if Omicron produces milder illness, especially for those who are vaccinated, the reopening of the economy would likely continue. In any case, the Fed and the markets will have considerably more information long before the Fed completes its bond buying program.

Investors and the Fed are increasingly concerned about inflation, with the Fed now likely to reduce its bond buying more quickly. This will enable it to start hiking policy rates sooner. Surprisingly, bond yields have declined, which we judge to be unsustainable. And inflation is likely to remain higher than the Fed’s target for some time, as the labor market is quite tight and wage rates are rising more quickly. Since labor represents the largest cost in producing GDP, any moderation in inflation from reduced bottlenecks is likely to be limited. So, we favor companies with tangible assets and business models that benefit from inflation, and we are keeping our bond durations short.

The foregoing content reflects the opinions of Advisors Capital Management, LLC and is subject to change at any time without notice. Content provided herein is for informational purposes only and should not be used or construed as investment advice or a recommendation regarding the purchase or sale of any security. There is no guarantee that the statements, opinions or forecasts provided herein will prove to be correct. Past performance may not be indicative of future results. Indices are not available for direct investment. Any investor who attempts to mimic the performance of an index would incur fees and expenses which would reduce returns. Securities investing involves risk, including the potential for loss of principal. There is no assurance that any investment plan or strategy will be successful.

Dr. Charles Lieberman is the Chief Investment Officer and co-founder of Advisors Capital Management, LLC. Dr. Lieberman began his professional career as an academic at the University of Maryland and Northwestern University. After five years in academia, he joined the…

About the Author… Read more

May you live in interesting times. Is that a blessing, or a curse? The day after Thanksgiving is notoriously boring in the stock market. It is a short, early close day, and typically volume is very light. Usually, nothing interesting happens. Since 1928, two-thirds of the 93 Black Fridays saw an average gain of 0.660% in the S&P 500, while one-third saw down days averaging -0.747%. Pretty boring, until, of course, Covid of the Omicron variety reared its ugly head. 2021’s edition of Black Friday saw the biggest day-after-Thanksgiving market decline in 90 years, second only to 1931’s 2.31% decline. Markets sold off sharply around the globe, commodities were slammed with crude oil taking the biggest hit (-13%) as investors reeled from the potential threat of a new virulent Covid strain. Are we doomed (again)?

Hand-in-hand with big market moves comes a spike in volatility, measured by the VIX, the CBOE Volatility Index. This index is commonly known as the Fear Index and measures the market’s expectation of volatility in the near future. Not surprisingly, the VIX leapt to its highest reading since May and ended the day at its highest level since February 25 and its sixth highest closing value of 2021. Below are two graphs of the VIX, the first represents the past year and the second is a long-term representation over 30 years.

VIX Year-to-date

VIX over 30 years

I would like to draw your attention to several points. Every time volatility has spiked and even stayed at an elevated level for a period of time, it has always subsided. Yes, it can stay elevated for months and years, but it has always returned to a more normal, or calm, level. Higher periods of volatility are frequently periods of extended market decline. Higher volatility equals higher fear. Fear peaked in October 2008, with the VIX measuring over 60 for most of the month, but the market didn’t find its bottom until March 6, 2009, when the VIX had dropped to the 40-50 range. Short-term jolts cause short-term corrections, while long-term trends take months to make themselves apparent. The point is that market sentiment takes a long time to change direction. Often (May 11-13, July 19-20, August 18-20, September 20-21 e.g.), short-term spikes subside just as quickly as they crop up.

The “potential” threat of the Omicron strain dealt a savage blow to crude oil prices as well as stocks. US crude fell more than $10 a barrel, or -13% on the day. While that move put a big dent in energy-related stocks, it also took a big chunk out of future gasoline prices. For drivers in California, where $5/gallon prices are common now, that’s decidedly good news. There are two sides to every equation.

Are we in an endless cycle of Covid mutation-flare up-lock down? I’m not a doctor, and I don’t play one on TV, so I can’t answer that question. What I do know about is investing in stocks. Stock prices go up and down. Fear levels go up and down. Investing in stocks is a pathway to financial goals and getting there is not a straight line. Indeed, stocks climb the Wall of Worry and the historical experience is that stock values move higher over time.

Call it a slap in the face or a wake-up call. It is good to get reminders occasionally that the market is not a linear progression. Risk matters and that’s why we at ACM take such care with our clients’ portfolios.

We live in interesting times and I’ll take that as a blessing.

The Risk-on, Risk-off Teeter Totter

The foregoing content reflects the opinions of Advisors Capital Management, LLC and is subject to change at any time without notice. Content provided herein is for informational purposes only and should not be used or construed as investment advice or a recommendation regarding the purchase or sale of any security. There is no guarantee that the statements, opinions or forecasts provided herein will prove to be correct. Past performance may not be indicative of future results. Indices are not available for direct investment. Any investor who attempts to mimic the performance of an index would incur fees and expenses which would reduce returns. Securities investing involves risk, including the potential for loss of principal. There is no assurance that any investment plan or strategy will be successful.

|

| Virtually every economic report we read these days refers to some form of slowing growth. Despite printing what would normally be a strong 6.5% quarter-on-quarter annualized rate in 2Q21, US GDP growth was almost 200 basis points below the consensus expectation.i In August, the University of Michigan’s consumer sentiment index fell to its lowest level since 2011, well below even the most pessimistic projection.ii In response to these and other notable misses, many economists and banks have revised down their forecasts for GDP growth for the rest of this year. Some more bearish market watchers even claim that the boogeyman of stagflation has returned to the US. Just look at how many recent stories on Bloomberg feature the term. |

|

||

|

|

||

| Source: Blackstone Investment Strategy and Bloomberg, as of 9/10/2021. |

| But it’s important to contextualize these macro figures. Just as the numbers posted last year frequently qualified as the “worst ever,” this spring and summer’s easy comps produced a series of eye-popping growth numbers, from services to manufacturing activity. Now that we’ve lapped the beginning of the US recovery, year-over-year changes are returning to earth. We discussed our expectation for volatile macro data in the June essay.

Areas of strain, including labor markets, global supply chains, China’s economic deceleration, and COVID-19, do merit concern. However, in my view, the fundamental strength of the economic rebound remains intact, powered by vaccine distribution and the US consumer. The recent growth slowdown is a speed bump on the road to recovery, not a treacherous detour. The distinction between the two has important portfolio implications. |

| Reasons for Concern |

| Labor market struggles Firms desperately need workers, but right now they’re simply not there. Nonfarm job openings have posted a new record in every month since March. In July, there were five job openings for every four unemployed Americans.iii The August NFIB Small Business Jobs Report revealed that a record-high 50% of all small business owners had job openings they could not fill, compared to the almost 50-year historical average of 22%.iv On the supply side of the market, labor force participation has hovered between 61.4% and 61.7% since June 2020, 1.6 percentage points lower than in February 2020.v And a record-high 3.98 million Americans quit their jobs in July.iii

Supply chain problems persist Global supply chains remain stretched, pushing up shipping and input costs and hampering inventories and production. Shipping capacity remains far too limited to satisfy rebounding demand, raising cargo prices to levels previously unimaginable. For example, a relatively small panamax class container ship fetched a daily charter rate of $200,000 in September; a couple of years ago, these ships were being sold for scrap.vi As Figure 2 shows, the spot rate to ship a 40-foot container from Shanghai to Los Angeles is now $12,424, more than eight times higher than pre-pandemic prices.vii And, several US port executives said they expect shipping logjams to continue at least through summer 2022, if not longer.viii |

|

||

|

|

||

| Source: Blackstone Investment Strategy, Bloomberg, and Drewry Supply Chain Advisors, as of 9/16/2021. Represents the spot container freight rate in US dollars for 40-foot container boxes shipped from Shanghai to Los Angeles. |

| Here at Blackstone, companies in our portfolio are seeing both labor and supply chain constraints materialize in real time. A number of CEOs of our portfolio companies reported in a 2Q’21 survey that, after COVID-19, they are focused on supply chains and the ability to hire and retain qualified workers. Surveyed CEOs in the US described annual inflation of about 4% across wages and raw materials. And an overwhelming majority of respondents to our survey whose firms experienced rising inflation and rates said that this could impact the performance of their companies.ix

The world’s second-largest economy slows down Two issues concern me with China. First, it appears the Delta variant precipitated the economy’s current slowdown. Previously, China led the global recovery due to its early actions to curb COVID’s spread. Now, its “zero-COVID” policy has shut down entire regions and sectors in response to small clusters of infections, disrupting many segments of the supply chain. For example, in the Ningbo port complex, the world’s third busiest port, an entire shipping terminal was closed due to one case, leaving dozens of cargo ships stranded.x China’s issues are unlikely to derail the US’s recovery, but further supply chain complications could damage global demand, especially in emerging markets that rely heavily on Chinese imports. The second issue is new regulation in the private sector. Perhaps one outcome of China’s slowing recovery will be a renewed focus on short-term growth numbers. But China tends to take a long-term view of domestic dynamics and develop methodological policy changes to effect desired outcomes. We should be prepared for the possibility that China may tolerate slower economic growth in exchange for bold reforms. 18 months later, COVID-19 lingers Our recent conversations with experts lead Byron and me to believe that Delta cases and hospitalizations in the southern US have probably peaked. Delta will likely now move north as the school year starts and as colder weather moves people indoors. Case numbers will rise, but hospital capacity in the Northeast should prove sufficient, largely thanks to those states’ higher vaccination rates. Globally, low availability of reliable vaccines in emerging markets poses a threat to their recoveries and increases the potential for further mutations of the virus. Our base case assumes that the transmission of future variants to the US and other highly vaccinated countries will be less damaging than Delta, as vaccinations and natural immunity will limit the spread. But, if a significantly more virulent or deadly strain were to develop, it could reduce the efficacy of current vaccines. |

| Reasons for Optimism |

| Vaccine uptake, efficacy point to continued recovery Thankfully, doctors, epidemiologists, and policymakers continue to make strides against COVID-19 and its variants. COVAX, a United Nations-backed program to distribute vaccines, is expected to deliver a total of 1.4 billion doses to 139 participating economies this year, with 1.1 billion of those doses being delivered between September and December.xi

Importantly, we know that the vaccines work. In the US, data from Washington state show that only 0.5% of fully vaccinated residents have contracted breakthrough infections. Just 9% of those cases required hospitalization.xii Vaccine efficacy is a major reason why I’m bullish on the US’s situation, especially in regions with strong vaccination rates and natural immunity. That includes California and New York City, two engines of the economy. Another positive is the coming Food & Drug Administration (FDA) approval of vaccine distribution to young children. Most importantly, this approval will protect our kids. But it will also increase parents’ willingness to return to normal activities, like dining indoors or going to the movies. The US consumer is a good bet My conviction in the US recovery is attributable largely to the consumer. We’re a nation of spenders, and we began this cycle from a position of historic strength due to low interest rates, pandemic debt forbearance programs, and generous government transfers over the past 18 months. Household net worth is at a record high in terms of absolute level and growth, compared to the five years it took to recover after the Financial Crisis. Meanwhile, the household debt service ratio, which tracks the amount of disposable income spent servicing mortgages and other forms of consumer debt, fell to 8.2% in 1Q21, its lowest level since tracking began in 1980.xiii This strength is evident on household ledgers. A JPMorgan Chase Institute study of over 1.7 million families who actively use checking accounts showed that median cash balances were more than 50% higher at the end of July 2021 compared to the same period in 2019. For families at all income levels, cash balances increased with each round of stimulus and remain elevated relative to pre-pandemic levels.xiv Firms spending again This cycle won’t just be powered by households. Much like consumer spending, capital expenditures experienced a dismal decade following the Financial Crisis. As prices, rates, and growth all struggled to recover, businesses had little incentive to invest for growth. But conditions are different today: the Fed’s measure of total capacity utilization is already back to its pre-COVID level.xv I think capital expenditures will break out in this cycle, driving up output and spurring healthy growth in the real economy. For example, according to The Economist, global tech firms will boost CapEx by 42% in 2021 relative to 2019.xvi |

|

||

|

|

||

| Source: Blackstone Investment Strategy and US Bureau of Economic Analysis, as of 6/30/2021. “Global Financial Crisis” is indexed to 100 as of 3Q07; “COVID-19 Crisis” is indexed to 100 as of 4Q19. |

| Investor Positioning for the Cycle |

| Real assets for a real recovery Investors should consider assets with exposure to the real economy, especially those that can benefit from an historically strong US consumer and rising business spending. This means housing and ancillary goods and services, which I discussed in my August essay. Concurrent housing and CapEx cycles are an unambiguous tailwind for US manufacturers, commodity producers, and energy firms. Another promising area is e-commerce, which claimed an increasingly large share of retail sales even before the pandemic pushed consumers online in droves.

Fed watch Thanks to quantitative easing, the Fed has purchased almost three-fourths of net Treasury issuance year-to-date, compared to just 5% of net issuance in 2019.xvii That level of demand makes it difficult to discern any kind of signal from rates markets about investor sentiment and economic fundamentals. But tapering will start soon, and the debt ceiling’s inevitable extension will free up greater debt issuance. In my view, the marginal reduction of Fed demand, combined with inflationary pressures that will prove stickier than the doves think, will likely lead interest rates to grind higher. That would deteriorate the value of cash and traditional fixed income products. But investors aren’t yet positioning their portfolios for that possibility, as fixed income prices remain elevated. The dollar value of global negative-yielding debt currently sits at $14.5 trillion, down from its December high but still an historical extreme.xviii In summary: Get cyclical I favor more cyclical positioning in equity and fixed income. That view flies in the face of recent weaker data, but I believe that lapping the recovery’s beginning has brought too much attention to data “misses” while obscuring high levels of activity in the real economy. While stagflation fears may keep making headlines, we are likely at the beginning of a consumer and business investment cycle that will drive secular outperformance among companies levered to the real economy and real assets. Additionally, I remain convinced that rates will grind higher, especially once tapering begins. That leads me to favor assets and sectors with positive exposure to interest rates, including financial stocks and short-duration or floating rate assets. There could also be potential opportunities in real estate, a sector which has historically featured strong current income and can return capital to investors in the near term for deployment in a higher-rate environment. We’ll take a closer look at market performance in the November essay, which will also feature insights from Prakash Melwani, Senior Managing Director at Blackstone and Chief Investment Officer of the Private Equity group. |

September has been a little bumpy, as history suggested it might be. As my colleague, Paul Broughton, wrote in a late August commentary (“Brace for September, But Don’t Panic”), investors needed to be prepared for the usual flow of negative news that seems to appear after summer vacations come to a close. There was plenty of bad news to go around over the last few weeks—from concerns about the debt ceiling to fiscal spending, higher taxes, and China’s issues. But, regardless, Paul wrote, fundamentals remain strong and investors would do well to focus on the longer term. But there’s been a lot of worry lately about that longer term, about future growth. Are we heading towards a lost decade, like in the 1970’s where stagflation took hold? Or are the facts showing a less worrisome trend? Remember, investors, you’re focused on the long term—at least a few years, right? So how does the real economy look and what should you be worried about?

Yes, growth is slowing. It has to, after the sharp recovery over the last few quarters from the pandemic’s shutdown across so many (especially, services) sectors. It now appears that real GDP growth will slow from an annualized rate of 12% last quarter to around 5% this quarter and 3% by the middle of next year. Note that those rates of growth are still comfortably above long-term GDP growth trends for a developed economy like ours (less than 2%). And yet we understand that all is not well and we “should” be growing faster. While we’re well off the bottom, there is presumably still some slack left.

It turns out it isn’t so easy to turn an economy back on after consumers and businesses went into hiding for a year. After a short hibernation in 2020, consumers came roaring back, looking to spend lots of extra savings, but businesses struggled to bring back workers and ramp up production. Consumers have been spending like it’s been Christmas for the last several months, but global production and shipping capacity is unable to handle it. Remember in years’ past when we’d suffer delayed deliveries in advance of the holidays? The shippers simply couldn’t add enough capacity for the holiday surge. Well, shippers have essentially been trying to deal with a holiday rush for the last several months. Ports are clogged, and so manufacturers, particularly out of China and southeast Asia, can’t get their products to those consumers.

Moreover, the producers can’t get enough parts to build the things consumers want – from cars to consumer electronics. The shortage in semiconductors is one very familiar example of those problems. Some expected those shortages to have abated by now, but we continue to hear of long backorders for those components. And that’s because it takes years, not months, to add new chip capacity.

Complicating matters further, is the delta variant. The surge in cases in the US and globally interrupted production, especially in APAC where so much of the world’s manufacturing takes place. Vietnam and Malaysia were particularly hard hit and that placed even greater pressure on China to deliver the goods. But China’s ports were already slowed by some delta-related shutdowns.

And then, finally, there are ongoing challenges among firms to fill open positions. It’s hard to ramp up production without enough workers. Many baby boomers chose to retire. And labor-saving technology investments can’t be made overnight. When people are reluctant to return to the workforce, for any number of reasons, it makes it harder to firms to get enough applicants to make good hires. That “matching” process can be slow in normal times. Add in concerns about delta or childcare and it only becomes slower.

So, are we facing stagflation, where inflation surges and growth stalls? Not likely, given the realities of strong demand and determined efforts to raise output. Look at the 1970s and early 80s in the chart below – that was stagflation. GDP growth went negative. Multiple times.

The outlook for the US economy isn’t anything like this (for one, we are unlikely to see the sort of negative productivity shocks we did in the 1970s from the OPEC oil embargoes). The shortages that are plaguing firms actually imply a longer recovery with GDP growth above normal for longer. Indeed, Bloomberg consensus forecasts (the shaded area in the chart) show that growth is not expected to stall out, but rather to remain above long-term trends for the next several quarters. But could inflation remain a persistent or even growing problem? While some shortages are likely to abate, which would reduce inflationary pressures, other shortages are likely to remain or even get worse, such as in housing and labor markets. So, a careful eye on that data is required, and we have positioned portfolios for the ongoing recovery potential and also to protect against the risk of higher inflation and interest rates.

The foregoing content reflects the opinions of Advisors Capital Management, LLC and is subject to change at any time without notice. Content provided herein is for informational purposes only and should not be used or construed as investment advice or a recommendation regarding the purchase or sale of any security. There is no guarantee that the statements, opinions or forecasts provided herein will prove to be correct. Past performance may not be indicative of future results. Indices are not available for direct investment. Any investor who attempts to mimic the performance of an index would incur fees and expenses which would reduce returns. Securities investing involves risk, including the potential for loss of principal. There is no assurance that any investment plan or strategy will be successful.

On the afternoon of September 11, 2001, I was flying back to Washington on Swissair Flight 128, returning home from a routine international bankers’ meeting in Switzerland. I’d been moving about the cabin when the chief of the security detail that escorted me on trips abroad, Bob Agnew, stopped me in the aisle. Bob is an ex-Secret Service man, friendly but not especially talkative. At that moment, he was looking grim. “Mr. Chairman,” he said quietly, “the captain needs to see you up front. Two planes have flown into the World Trade Center.” I must have had a quizzical look on my face because he added, “I’m not joking.”

In the cockpit, the captain appeared quite nervous. He told us there had been a terrible attack against our country—several airliners had been hijacked and two flown into the World Trade Center and one into the Pentagon. Another plane was missing. That was all the information he had, he said in his slightly accented English. We were returning to Zurich, and he was not going to announce the reason to the other passengers.

“Do we have to go back?” I asked. “Can we land in Canada?” He said no, his orders were to head to Zurich.

I went back to my seat as the captain announced that air traffic control had directed us to Zurich. The phones on the seats immediately became jammed, and I couldn’t get through to the ground. The Federal Reserve colleagues who had been with me in Switzerland that weekend were already on other flights. So with no way to know how events were developing, I had nothing to do but think for the next three and a half hours. I looked out the window, the work I’d brought along, the piles of memos and economic reports, forgotten in my bag. Were these attacks the beginning of some wider conspiracy?

The question I focused on was whether the economy would be damaged. The possible economic crises were all too evident. The worst, which I thought highly unlikely, would be a collapse of the financial system. The Federal Reserve is in charge of the electronic payment systems that transfer trillions of dollars daily in money and securities between banks all over the country and much of the rest of the world. We’d always thought that if you wanted to cripple the U.S. economy, you’d take out the payment systems. Banks would be forced to fall back on inefficient physical transfers of money. Businesses would resort to barter and-IOUs; the level of economic activity across the country could drop like a rock.

Yet even as I thought about it, I doubted that physically disrupting the financial system was what the hijackers had in mind. Much more likely, this was meant to be a symbolic act of violence against capitalist America—like the bomb

in the parking garage of the World Trade Center eight years earlier. What worried me was the fear such an attack would create—especially if there were additional attacks to come. In an economy as sophisticated as ours, people have to interact and exchange goods and services constantly, and the division of labor is so finely articulated that every household depends on commerce simply to survive. If people withdraw from everyday economic life—if investors dump their stocks, or businesspeople back away from trades, or citizens stay home for fear of going to malls and being exposed to suicide bombers—there’s a snowball effect. It’s the psychology that leads to panics and recessions. A shock like the one we’d just sustained could cause a massive withdrawal from, and major contraction in, economic activity. The misery could multiply.

Long before my flight touched down, I’d concluded that the world was about to change in ways that I could not yet define. The complacency we Americans had embraced for the decade following the end of the cold war had just been shattered.

In late September, the first hard data came in. Typically, the earliest clear indicator of what’s happening to the economy is the number of new claims for unemployment benefits a statistic compiled each week by the Department of Labor. For the third week of the month, claims topped 450,000, about 13 percent above their level in late August. The figure confirmed the extent and seriousness of the hardships we’d been seeing in news reports about people who’d lost their jobs. I could imagine those thousands of hotel and resort workers and others now in limbo not knowing how they would support themselves and their families. I was coming to the view that the economy was not going to bounce back quickly. The shock was severe enough that even a highly flexible economy would have difficulty dealing with it.

But while the immediate shocks were significant, the economy righted itself. Industrial production, after just one more month of mild decline, bottomed out in November. By December the economy was growing again, and jobless claims dropped back and stabilized at their pre-9/11 level. The Fed did have a hand in that, but it was only by stepping up what we’d been doing before 9/11, cutting interest rates to make it easier for people to borrow and spend. I didn’t mind seeing my expectations upset, because the economy’s remarkable response to the aftermath of 9/11 was proof of an enormously important fact: our economy had become highly resilient. After those first awful weeks, America’s households and businesses recovered. What had generated such an unprecedented degree of economic flexibility?

Economists have been trying to answer questions like that since the days of Adam Smith. We think we have our hands full today trying to comprehend our globalized economy. But Smith had to invent economics almost from scratch as a way to reckon with the development of complex market economies in the eighteenth century. I’m hardly Adam Smith, but I’ve got the same inquisitiveness about understanding the broad forces that define our age. After 9/11 I knew, if I needed further reinforcement, that we are living in a new world-the world of a global capitalist economy that is vastly more flexible, resilient, open, self-correcting, and fast-changing than it was even a quarter century earlier. It’s a world that presents us with enormous new possibilities but also enormous new challenges.

While the economic impacts of 9/11 were short-lived, the forces behind the 9/11 terrorist attacks have hardly evaporated. As the Biden Administration’s unbalanced withdrawal from Afghanistan recently demonstrated, the Taliban are still very much in play. Who’s to say what international crisis they could engender? Could a 9/11-type attack happen again? Perhaps. Though I’d like to think that our intelligence community and the advances in surveillance over the past 20 years have given us a greater awareness of the threats we face. In fact many threats we’ve faced since 9/11 have been thwarted by just those advancements.

While the world has changed in many ways since 9/11, the one thing that has not changed is human nature. Tying in to my August newsletter, fear remains a dominant force in our economy. Economic contraction following any major event—9/11, the 2008 financial crisis, and most recently the onset of the COVID pandemic—is driven most forcefully by fear.

While fear is indeed a clear driver of economic contraction, as we’ve witnessed over the past year and a half, resilience is also a part of human nature that has the ability to counteract fear-driven economic contractions. They say necessity is the mother of invention, and when faced with a once-in-a-lifetime pandemic it was, yet again, human ingenuity that kept the economy from falling apart. The solutions we have developed in response to the pandemic will undoubtedly shape our future, especially as processes intended to be temporary become more mainstream and enduring. The innovations in communications technology that allowed work to be decentralized away from a physical office will affect how we live long after COVID is tamed. The mRNA technology that allowed a vaccine to be developed in record time has the potential to combat other infectious diseases and even treat cancer. As we continue to recover from this most recent crisis, I look forward with optimism and the belief that the challenges we overcome and the ingenuity humanity possesses ultimately make us stronger.

The foregoing content reflects the opinions of Advisors Capital Management, LLC and is subject to change at any time without notice. Content provided herein is for informational purposes only and should not be used or construed as investment advice or a recommendation regarding the purchase or sale of any security. There is no guarantee that the statements, opinions or forecasts provided herein will prove to be correct. Past performance may not be indicative of future results. Indices are not available for direct investment. Any investor who attempts to mimic the performance of an index would incur fees and expenses which would reduce returns. Securities investing involves risk, including the potential for loss of principal. There is no assurance that any investment plan or strategy will be successful.

LATEST ARTICLES