The Impact of Covid in Europe

Target2 (Trans-European Automated Real-time Gross Settlement Express Transfer System) is the clearinghouse for the Eurozone’s central banks. It is a centralized payment system which enables both central and commercial banks to process euro payments in real-time.

Target2 replaced the Eurozone’s original “Target” system beginning in 2007 as a more secure and efficient real-time gross settlement (RTGS) system than its predecessor. TARGET2 reduces risk inherent in cross-border payment transactions by providing a central clearinghouse for such transactions. This helps to provide financial stability and financial integration in the euro area and supports the European Central Bank’s single monetary policy. According to the Deutsche Bundesbank (Germany’s central bank), Target2 processes around 350,000 payments with a value of about €1.7 trillion each working day, amounting to 90 million payments with a value of about €430 trillion per year.

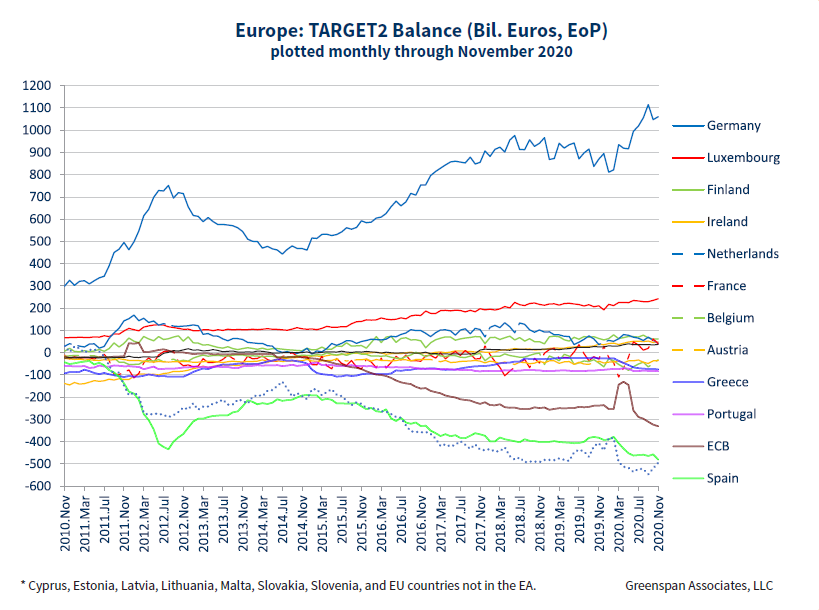

Target2 is an important financial concept to examine because of what it tells us about the disparity between northern and southern Europe and the long-term challenges possibly facing the stability of the Eurozone. First, we examine Target2 balances by country:

The above chart shows the balance of payments for Europe’s TARGET2. One can see the massive disparity where the Deutsche Bundesbank’s balance is so much larger, by far, than that of every other country. Also of note is that the European Central Bank (ECB) itself is a net borrower. Germany is effectively funding much of Europe, especially southern Europe, and I’m not sure how sustainable such a relationship is.

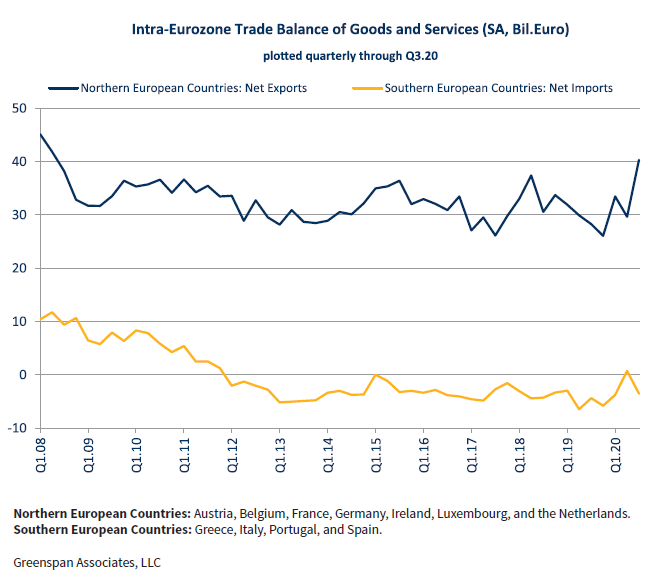

Before the adoption of the euro as a common currency, these trade imbalances would have been ameliorated by currency exchange rates. If Italy were running large trade deficits against Germany, for example, the lira would fall in value relative to the Deutschmark. This would improve Italian exporters’ competitive position as Italian goods would appear less expensive and exports would increase. With a common currency, exchange rates are locked and cannot compensate for differences in competitiveness amongst Europe’s economies. This dynamic has led to a dichotomy in Europe where northern countries habitually run surpluses against their southern compatriots:

The COVID-19 pandemic has further exacerbated Europe’s internal imbalances. Germany’s Target2 balance has grown significantly since March 2020 largely due to the expansion of Eurozone purchase programs in response to the COVID-19 pandemic. Bundesbank experts suggest that there may be other monetary policy operations like a series of targeted longer-term refinancing operations (TLTROs) which might also have increased Target2 balances. But the increase in liabilities on the parts of southern European countries like Italy and Spain since March 2020 is undeniable. In December alone, Italy’s Target2 liability jumped by more than €20 billion.

At present, the Bundesbank acknowledges Germany’s large TARGET2 balance but deflects that this “would only ever pose a risk if a country with a negative balance were to leave the euro area.” If a country were to leave, and furthermore default on its obligations, the write-off would be borne proportionately by the remaining members. At the height of the Greek debt crisis, when speculation Greece may leave the euro area roiled financial markets, its TARGET2 balance stood at about negative €100 billion. Today, the balances of Italy and Spain are around negative €500 billion each. How long Germany can stand to be the creditor of Europe, and what amount Germany is willing to risk, may become a significant issue.

About the Author

Dr. Alan Greenspan

Alan Greenspan served five terms as chairman of the Board of Governors of the Federal Reserve System from August 11, 1987, when he was first appointed by President Ronald Reagan. His last term ended on January 31, 2006. He was…

LATEST ARTICLES